4 TIPS TO REDUCE THE RISK OF A DISASTER IN YOUR BUSINESS

Accidents tend to happen even if we try our level best to prevent them. An employee may get injured, a fire may occur and end up damaging your office space, and a cyber-attack leads to a data breach. Unexpected emergencies can shut down your operations for hours, days, or even weeks with a potentially serious impact on customer relationships and revenue. Is your company prepared to handle these kinds of disasters?

Benjamin Franklin once said: “By failing to prepare, you are preparing to fail.” And in this case, it is true when it comes to business emergencies, studies show that more than 40% of small businesses close permanently after a disaster.

If you plan to protect your business against some of the most catastrophic or shocking potential disasters, pay attention to the following:

- Fraud. Your business could be defrauded in a number of ways pay attention to customers and business partnerships promising great long-term benefits that might be misleading and may never pan out. Secondly, internally your trust in your team should not mean that you don’t verify what they do they maybe misappropriate funds from your business or even worse send your contracts and partner clients to your competition. Always pay close attention to the finance and procurement teams and any other team member dealing directly with your clients.

- Cash flow interruptions. Cash is King in a business; Paying attention to your Cash runway means the number of months your business can keep operating before it’s out of money. So as not to run into cash flow problem its paramount to pay attention to incoming cash and outgoing cash always. Look out for drop in expected revenues get to the root cause which product is not selling why, a customer who won’t pay on time etc.

- Intellectual property lawsuits. As much as possible verify your work multiple times to ensure you are not plagiarizing another company. pay attention to images you use consent for pictures used in your blogs mentions of other companies and brands in adverts ensure you have consent.

- Personal injury lawsuits. Personal injuries in the workplace are they could happen. Lower this risk by establishing stricter, more comprehensive safety requirements, insisting on a protective waiver or similar legal document for your customers, and even obtaining litigation insurance so as to minimize your company’s vulnerability.

- Natural disasters. your business could be susceptible to floods, fire, earthquakes, pandemics, and plagues, this may jeopardize your business and cost you lots of cash and time to replace what has been destroyed Be proactive and get the insurance that covers disasters and property damage.

- Scandals: Bad news spreads quickly especially now in the digital era we live in. Financial Scandals get more attention especially when consumers of your product or service are going to be impacted. if your products malfunctions consumers may cause an uprising. It’s important to remain as transparent and accommodating as possible when this happens and be proactive in letting the consumers know what you are doing about it.

It’s impossible to prepare for everything that might go wrong in your business some situations are unpredictable. It’s important to hedge and prepare for the possibilities of the imagined possible scenarios and create a contingency plan.

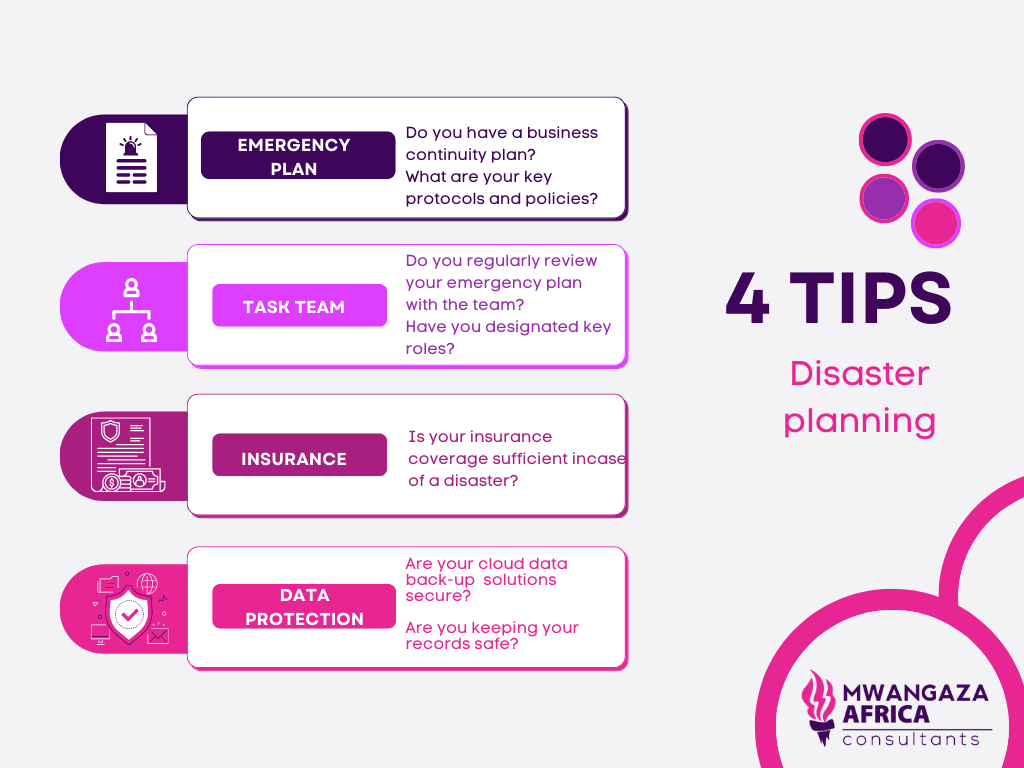

Here are the 4 tips to help you mitigate disasters in your business.

1. CREATE AN EMERGENCY PLAN

The first step in creating an emergency plan for your business is to assess the primary risks that could take place in your business, whether that will be weather, cyber, equipment-related or internal human resource risks.

It’s important to formulate primary goals for your plan, which should at least, be able to protect employees, eliminate any immediate dangers such as chemical leaks or faulty equipment and keep your business running as smoothly as possible. Make sure to address the key plan aspects of your plans with your team, such as a list of employees to contact during an emergency, building evacuation policies, as well as those that are responsible for managing essential protocols during emergencies.

2. PREPARE A TASK TEAM

A plan is only as effective as the people who are implementing it. Make sure to clearly set out the responsibilities of each employee. who is communicating to stakeholders about your disaster what information is to be shared with consumers have a list of all your suppliers and customers with contact details to be able to communicate to them on your next steps and reassure them of your service to your consumers.

Be thorough in reviewing and rehearsing your plan with your task team members. This should be done at least twice a year to keep disaster management a priority for your team.

3. REVIEW THE INSURANCE COVER.

Based on your business’s risk assessment and emergency plan, the next step is to have a conversation with your insurance agent, who can then help to determine the level of insurance coverage that will be the most suitable for your business from protecting against disasters such as equipment breakdowns, theft, or natural calamities, litigation, fire. Many businesses usually underestimate the amount of coverage they need, only to learn later that a particular disaster was not covered under their policy.

4. PROTECT YOUR DATA

Today’s digital world is growing at a very fast rate, and hacking and computer viruses continue to be major issues that can result in not only physical and financial loss but also emotional distress. Data that is stored electronically also faces several threats, from mechanical malfunctions and phishing to natural disasters that can damage or destroy hard drives or paper files with vital information. Therefore, it is very important to invest in cloud-based solutions, which offer secure data that is accessible from any location. If you are not storing data in the cloud yet, be sure that you digitally back up and encrypt important data frequently in a location that has a good distance from your business headquarters. Paper documents such as contracts, licenses, and corporate records can be stored in a fireproof box or a bank safety deposit box. It is also vital to have data breach protection and remedies in place that protects you from identity theft.

SUMMARY.

More than 40% of small businesses close permanently after a disaster. Unexpected emergencies can kill your operations for hours, days, or even weeks. Is your company prepared to handle these kinds of disasters? Here are four tips to help you plan for common business disasters. Hackers and computer viruses are major issues that can result in physical and financial loss.

Data that is stored electronically also faces several threats, from mechanical malfunctions and phishing. It is very important to invest in cloud-based solutions that offer secure data accessible from any location.

Author:

P Wakesho & K . Wahome